B2B Payments Don't Have a Problem. They Have Twenty-Three. (1 of 5)

Part 1 of 5 Exploring B2B Payment Challenges

Having worked in B2B payments for nearly thirty years, I’ve watched brilliant people, well-funded companies, and genuine technological advances approach this space from every angle. There’s been progress. And yet, the same systemic problems facing my clients in the early 2000s continue to haunt them today.

Why? I think it’s because the industry has consistently discussed the “B2B payment challenge” as if it were one problem. It isn’t. It’s a collection of distinct pain points — I count at least 23 — that cluster into six categories. And understanding which type of problem you’re dealing with is what determines whether a given solution can address it, or whether it’s just going to shift the pain (and call that progress).

This post introduces a framework to understand and categorize B2B challenges. The rest of the series will work through it, and recommend some actionable strategies along the way.

First, a brief orientation

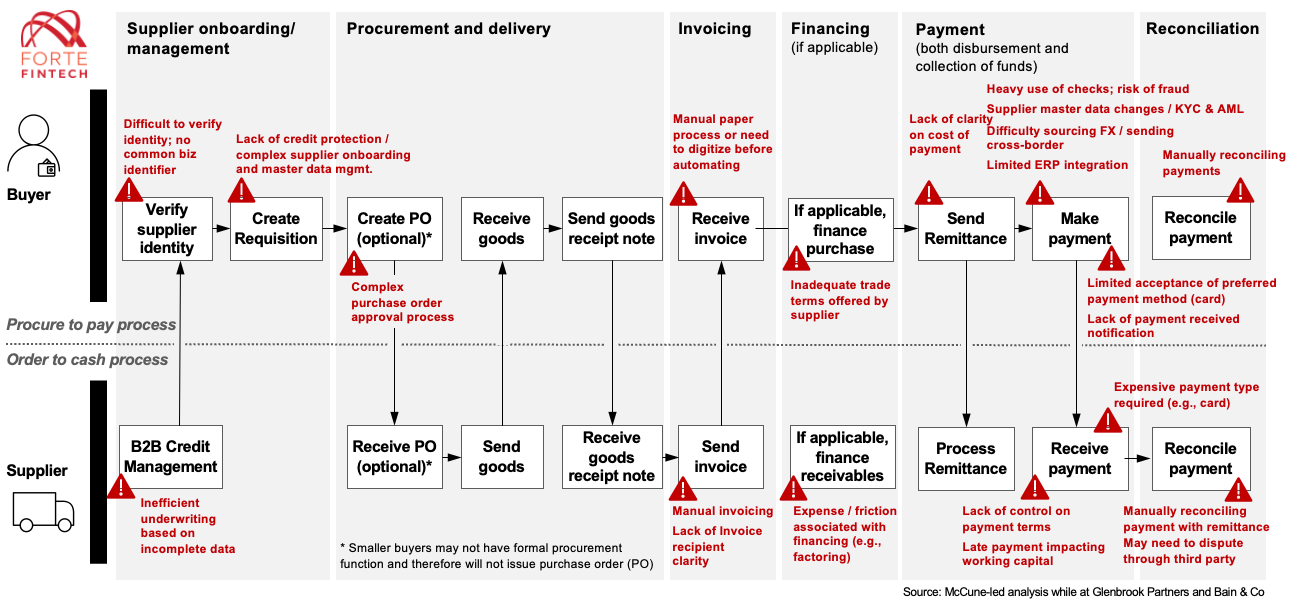

A B2B payment doesn’t happen in isolation. It’s the culmination of a long chain of business processes that starts well before any money moves and continues after it does.

On the buyer side, that chain runs from supplier sourcing and onboarding through procurement, receipt of goods or services, invoice processing and approval, payment disbursement, and finally reconciliation. On the supplier side, it’s the mirror image: onboarding with the buyer, fulfilling the order, generating and sending an invoice, managing the financing of receivables if needed, receiving and applying the payment, and reconciling everything in the AR system.

These two chains — the buyer’s procure-to-pay cycle and the supplier’s order-to-cash cycle — are interdependent and deeply intertwined. Every step in one generates an action or a data requirement in the other. The payment itself, the thing our industry spends most of its time discussing, is merely one step. And the likelihood of that payment being for the right amount, on time, and with relevant accompanying data is often dependent on all the other processes.

Thus B2B payment challenges are distributed across the entire lifecycle. An identity verification failure at supplier onboarding creates problems that resurface at payment. A purchase order that doesn’t make it to the right person at the supplier creates exceptions weeks later. Remittance details that get stripped from a payment land on an AR clerk’s desk as a manual matching and reconciliation task. If you only look at the payment step, you see maybe a third of what’s actually broken.

Over many years of consulting work — and, I’ll confess, an embarrassing number of iterations of the same slide (pictured below) — I’ve mapped the challenges that buyers and suppliers face across this lifecycle.

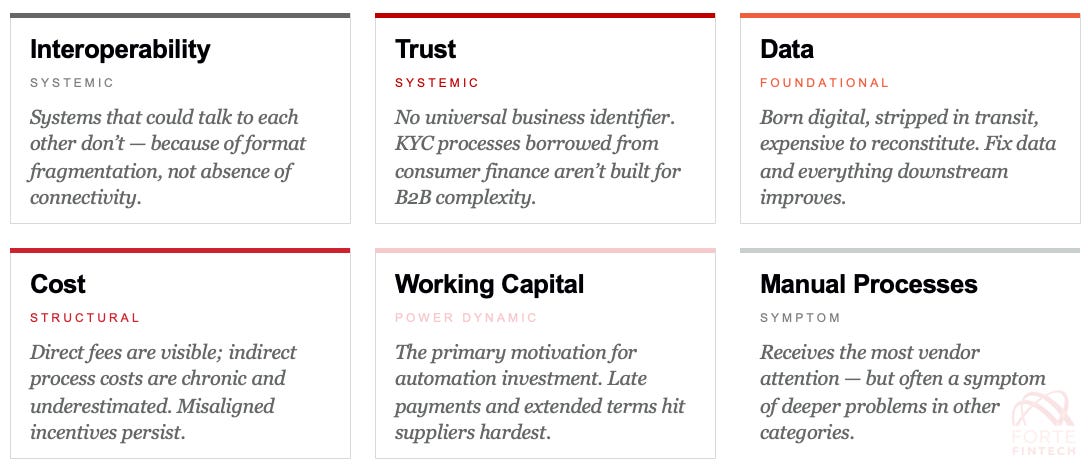

Six categories of challenge

After several years discussing this slide, I finally got around to mapping the 23+ specific challenges into buckets and was struck by just how convoluted and nuanced the issues really are. The challenges fall into six categories:

Interoperability is fundamentally an infrastructure problem. Buyers and suppliers use different Office of the CFO (aka OCFO) software systems, run on different payment processors, and communicate through different formats. Purchase orders leave one system and arrive in another in a format that requires ingesting documents or manual re-entry. Payments travel without the remittance data needed to apply them. Systems that could theoretically talk to each other don’t, ironically because we have a profusion of standards, connections, and integrations. This is a systemic, ecosystem-level challenge. Interoperability gaps create work and errors both down- and upstream.

Trust is a compounding problem. Before they transact, businesses must verify each other’s identities, assess creditworthiness, screen for fraud and regulatory risk, and then maintain/update that knowledge over time as they buy and sell from one another on an ongoing basis. There is no universal business identifier. KYC (know your customer) processes borrowed from consumer finance aren’t quite right for B2B. We actually need KYB (know your business) processes validating the legitimacy of the entity, while also maintaining KYC on beneficial owners for AML purposes. Businesses operate across jurisdictions and have complicated legal structures, often involving subsidiaries. And we haven’t even considered fraud yet…

Data is the original sin. In 98% of B2B scenarios, it was born digital, got stripped or detached in transit, and now requires expensive work to reconstitute. Invoice data re-keyed rather than transmitted. Remittance separated from payment. Payment confirmations that arrive without enough information to match to an open receivable. I often quip, moving the money is easy, it’s the data that’s the problem! Fix data and reconciliation gets easier, underwriting improves, and automation becomes reliable rather than aspirational.

Cost challenges reveal misaligned incentives. There are direct transaction costs — interchange fees, FX spreads, factoring discounts — that are visible on statements and negotiated explicitly. And there are indirect process costs — the labor, errors, delays, and manual workarounds that accumulate across hundreds of employees’ working hours — that are chronically underestimated. Treasury decision makers optimizing for low transaction fees (e.g., ACH) are not the accounting team that absorbs the process costs of those transactions (remittance via email). The relative expense of B2B card transactions, not baked into pricing structures as they have been for consumer purchasing, is borne by suppliers. That cost funds rebates that their buyers benefit from. That misalignment has cast a halo of resistance to B2B payment digitization in general.

Working capital is the primary motivation for back office automation. Businesses invest in digitizing in hopes of receiving more accurate and timely signals to manage their day-to-day and strategic investing and borrowing. Late payments, inadequate payment terms, and expensive financing challenges are often the effect of failures and inefficiency in other categories. When a buyer faces working capital pressure, the easiest thing to do is to extend payment terms. This is rational behavior in the face of uncertainty. Suppliers, especially smaller ones, have much less leverage and struggle disproportionately.

Manual processes is the category that gets the most vendor attention for obvious reasons. Receipt, digitization, and processing of invoices was an early and important B2B achievement. We have mature AP and procurement processes for buyers and sophisticated billing solutions that enable every conceivable business model. Yet decades on, we’re still optimizing OCR, grappling with manual exception handling, and chasing down stray invoices and remittance information. And that’s just the activity between buyers and suppliers. Within back offices, accounting and finance teams struggle with awkward manual download, Excel (!) manipulation, and uploaded handoffs between the various software tools they rely on. We’ve made tremendous progress — and we have a ways to go. “Straight-through processing” remains stubbornly elusive. An important caveat, which I’ll return to throughout this series, is the truism that automating a broken process doesn’t fix the underlying issues and in fact often amplifies the scale of the problem.

The most impactful interventions in B2B payments address multiple categories simultaneously. But they’re harder to build, harder to sell, and harder to implement. Which is why they’re rare.

Illustrating the framework: checks

Consider the persistent use of checks for U.S. B2B payments as an illustration of the framework. This stubbornly persistent phenomenon1 remains the subject of endless vendor campaigns.

Checks persist because they simultaneously solve for all six challenge categories in ways that electronic alternatives have struggled to match. Checks carry remittance data with them in the envelope (data). There are fraud-resistant means to protect high-value B2B transactions when paired with bank controls such as positive pay (trust). The infrastructure around them, including wholesale lockbox services, had evolved over decades so that today image check processing is the norm and once deposited, checks clear same day. Checks have widespread reach becuase every business can receive a check and legacy software solutions were all designed for an era of batched check payments (interoperability). Relatively few businesses still manually write checks (manual processes) because software providers and banks handle ‘check runs’ for them. Despite speeding up the processing and settlement, mail float remains an attractive motivation for many old school B2B payment decision makers (working capital). Finally, the indirect process costs of checks are largely baked in to the back office status quo (cost).

[Confession: Early in my career I was involved in the intial efforts to commercialize image check processing (in the late 1990s — pre-Check 21!). The unintended consequence has been that checks are more efficient and harder to get rid of. I’ve been trying to make up for it ever since.]

What comes next

In the posts that follow, I’ll work through the implications of this framework systematically.

Post 2 looks at how the pain is distributed between buyers and suppliers — and loudly proclaims the uncomfortable fact that our industry offers fewer benefits for suppliers, and has in many cases made things worse for them.

Post 3 goes category by category, asking what the nature of each problem tells us about the kind of solution it requires. Some of these problems are systemic challenges that no single company can solve. Others are data problems that the latest generation of AI tools may finally be able to address. Still others are power dynamics dressed up as efficiency problems that no amount of software investment will change.

Post 4 draws strategic implications: who is well-positioned for an era of interoperability, what the competitive and cooperative dynamics look like, and why I think most “B2B networks” are fantasies.

Post 5 is where I let myself be uncharacteristically optimistic. Agentic AI is generating a lot of hype, some of it deserved. I want to be specific about where I think it can move the needle across all six categories — and honest about where the limits are.

Nearly thirty years in, I still find this space interesting. That’s either a sign of genuine intellectual depth or an alarmingly naive optimism. Possibly both.

Which of these six categories do you think has been most neglected — by payment incumbents like banks and card networks, by software vendors, by the analysts? I have a strong view. I’m curious whether it matches yours.

This is Part 1 in the Exploring B2B Payment Challenges series. Part 2: Our Approach to B2B Payments Is Asymmetrical →

We have made progress! In 2004 checks represented 81% of U.S. B2B payments. As of 2025 we’re down to 26%. Source: AFP & Nacha

Great foray into Substack, with a cliffhanger on post one. Now we have to follow the whole series (not that we wouldn’t anyway).

I’m biased, but I’d double-click on Data as the real battleground. It’s the one category that hasn’t been “papered over” with shiny workarounds (like virtual cards tried to be a solution to everything… and mostly became a solution to their own business model).

Manual Processes aren’t quite the same kind of category. They’re the result of fragmentation—when data and processes don’t connect, humans become the integration layer.